Quitting my job

Quitting my job

Closing one door so that another may open

Today is a big day for me, and one that I’ve been planning for some time: I’m stepping down from my current position in information technology support and engineering to pursue opportunities in the cryptocurrency and blockchain space. I don’t actually have anything lined up at the moment, but am instead taking a hiatus to spend some time with my family and focus on building smart contract applications and decentralized organizations.

I’ve been planning this move for almost three years, after my first bitcoin bull run, but the inertia of comfort has been a hard one to overcome and I figured the only way for me to actually do the thing I wanted to do was make a clean break and quit. So three months ago I gave my now-former boss, Pat Kelly, ninety days' notice and started preparing.

I’m grateful to him for the opportunity he’s given me the past eight and a half years. We’ve watched our kids grow up, and he’s put up with me while I worked on various political campaigns and finished my college degree. When he hired me I had just been fired from my previous job and had a three-month old baby at home to feed. I’m in a much different place today, and it’s time that I move on.

Parenting from home

The world is in a much different place now as well, and while there appears to be signs of normalcy returning as the COVID pandemic winds down, I’m not in any hurry to return to the status quo, if indeed we ever will. I’ve written about my experience parenting at-home these last eighteen months, and despite the challenges, I’m in no hurry to send the little ones off to school in the fall. In fact, there’s a part of me that wants to opt them out of the public education system entirely and explore “alternative” options, some of which we’ll be experimenting with over the summer.

Stacy recently remarked that she never imagined I’d make such a good preschool teacher for Harper, who I’ve been teaching reading, writing, and math. She’ll most likely be attending Kindergarten in the fall, but I’ll be enrolling Berkley, who’s finishing third grade in the next week, in GalileoXP, an online self-directed education platform. If she takes to it, and can convince my wife, I’m more than happy to let her stay home with me and work with kids from around the world as she learns entrepreneurship, coding, writing, crafts, or whatever subject her heart directs her toward. I want her to have the freedom to start choosing her own path, and frankly, I don’t think that teaching her how to do well on the Standards of Learning is going to prepare her for a career in the 2030’s.

Future Shock

During the waning months of the Trump administration, I remember someone saying that the “2030’s came early.” They were referring to the way that most knowledge workers had transitioned to work from home basically overnight, but I think it’s a relevant insight about the increasing rate of change that we are experiencing in ever shorter time frames. Alvin Toffler wrote about it in Future Shock, written in the seventies, and I’ve been waiting for the technological singularity, predicted in Ray Kurzweil’s 1990’s book to occur between 2020 and 2040. Kurzweil’s The Singularity Is Near predicted an era in which the advent of general artificial intelligence surpasses the ability of mankind to keep pace with what’s going on. I might argue that in some ways we’re already there, that as sci-fi author William Gibson wrote decades ago: “the future is already here, it’s just not evenly distributed.”

Part of this explains my disillusionment with traditional power structures and ways of organizing labor and capital. We can leave aside my failed political aspirations here for the moment, please, but I’ve come to a deep belief that our current governmental structures are ill-suited to respond to the current crises at hand. Our inability to deal with the climate crisis is one obvious example, but the global response to the pandemic should have shed any doubts that political systems designed in the eighteenth century are capable of dealing with the challenges of the twenty-first. Congress still can’t figure out what to do about Facebook and Google. So while I might make an exception for local governments, tech companies currently have more of an effect on our day to day lives. That’s not to say that I have any faith that Bezos, Musk or Zuckerberg are going to rescue humanity from our baser instincts either. Quite the opposite, as we’ve seen.

Crypto, DeFi and Daos, oh my!

That said, I think the experiments that are going on in the decentralized finance space, DeFi as it’s called, are quite amazing. One can think of smart contracts as public, decentralized, censorship resistant, immutable, cryptographic computer programs that can hold money. The fintech industry is undergoing a revolution right now, these networks are basically black holes for capital and talent, and it's moving so fast that it's a sight to behold. DeFi protocols have been described as money legos, and they’re being combined in ways that are going to disrupt most of the traditional “too big to fail” finance system in the next five to ten years. This is one area I’m focusing on.

The second, closely related to DeFi, are called decentralized autonomous organizations, or daos. They’re basically democratic organizations, organized on blockchains, with rules written into smart contracts. Think if Robert’s Rules of Order were written into a computer program. These daos can be organized as corporations, or non-profits, venture firms, or charitable foundations. The point is that with a few exceptions, these daos exist outside of the operational jurisdiction of any government. Smart contracts aren’t taxable, and I think that by the time governments catch on to what’s happening it’ll be too late.

That’s not to say that dao participants aren’t beholden to their home jurisdictions, nor that daos are the perfect democratic organizations. I will venture that as blockchain wallets, which are inherently anonymous, become the primary means for interacting with websites and services, we will see more and more individuals organizing within these new shadow governance structures, opting out of traditional corporate and civic organizations.

Going all-in

The reaction that I get from my friends and family when I tell them I’m “retiring”, is one of skepticism, doubt, and incredulousness. The only other people who seem to understand are those involved with crypto themselves, those who have gone through similar plans or aspire to. Everyone else seems to think I’m crazy.

“It’s good to have plans,” a colleague told me weeks ago.

“No one ever lost money selling,” a relative told me, urging me to de-risk my positions and sell back into dollars, noting that “anything can happen”, alluding to bitcoin’s infamous price cycles and notorious eighty percent corrections.

Last March, the black swan of the COVID lockdown caused a dump in the bitcoin and equity markets, sending bitcoin down 50% in a single day. Since this Black Thursday the price of bitcoin has rebounded some two thousand percent. Since its inception twelve years ago, bitcoin’s price has appreciated over 200% annually, making it the best performing asset of the last decade. And while the crypto markets did see another pullback of some forty-fifty percent last week, wiping out billions of dollars of leverage position in the process, there’s been little change in on-chain metrics and broader macroeconomic pictures, which shows little indication that we’re anywhere near the end of a bull market.

In fact, this current run seems a bit understated compared to the mania that occurred in late 2017, so my sense is that we’ve just gotten started. There’s been a lot of speculation among bitcoiners as to where this cycle’s top will be, the more “conservative” estimates and predictions are well over six figures, with some analysts anticipating a spike to $200,000 or higher before the end of the year. Also, some are questioning whether this might be a “supercycle”, near the plateau of the adoption S-curve, and that we’ll see even higher prices with less volatility moving forward. Earlier this year bitcoin reached a one trillion dollar market cap, and there are signs that many institutions are adopting bitcoin, not gold, as a hedge against inflation. If bitcoin is able to flip gold as some anticipate, then there are very strong cases for a $500,000 or even $1,000,000 price per bitcoin in the next five to ten years.

And if you hesitate to believe that, then I have three words for you...

Modern monetary theory

The financial response to the COVID pandemic has been an unprecedented amount of money printing by the Federal Reserve and other central banks. Somewhere around thirty to forty percent of all US dollars currently in circulation were printed in the last year, and the figures are similar for most other currencies. This quantitative easing has led to noticeable biflation as the equity and real estate markets have skyrocketed. Now, with post-pandemic economic demand growing and what amounts to universal basic income checks on the way, it seems that supply and demand are leading to a surge in energy and other commodity prices.

Measured inflation, via the CPI, has been trending near zero, the Fed has been hell-bent on a two percent target, with Chairman Powell floating the idea to let things “run hot” to make up for lost time. The most recent quarterly inflation figures showed a higher than expected rise, adding to fears that the US might be headed to a repeat of 1970’s interest rates, or worse, an end to the current post-war business cycle. While the Biden administration's current budget plan is to spend its way out of the current economic situation and stimulate growth, the realization among bitcoiners and Austrian economists is that the only real long term solution to the current debt to GDP ratio is debasement of the dollar.

The Wiemar Republic seems to be a favorite subject lately among those eyeing the macroeconomic environment. When Money Dies, a book about the collapse of the German mark in 1923, seems to be on everyone’s reading list as people look to the Nigerian, Venezuelan, and Argentinian economies and wonder if it can happen here. It is not an easy read, but it is a fascinating one, and while I was dumbfounded by most of what I read, I still could not help noting the parts of its history that had parallels to recent events. Mainly, the inability of the Wiemar government to be able to recognize that the cause of their ongoing inflationary troubles was not the lack of marks available, but that there were too many of them in circulation.

Infinite demand for scarce assets

Anyone paying attention to the housing and construction markets the last year or so has witnessed the effect of this influx of stimulus checks and QE. In my neighborhood, houses have sold the day that they’re listed, and my friends in the real estate industry have been making money hand over fist. Some of this is due to demand for lumber (home improvements) as well as tech workers fleeing high priced housing in San Francisco and elsewhere as part of work from home, but much of it is due to the Cantillion effect. Basically what it means is that when money is printed by the government, via QE or stimulus check, most of the immediate benefit goes to the well off, who don’t need it for day to day expenses and instead invest it. As stock market equities have reached ludicrous heights, some pension funds, high-net-worth individuals and other smart money has started looking elsewhere, namely the real estate market.

As Americans who currently live under the world’s reserve currency, we’re in a sheltered position, but eventually all fiat currencies trend toward zero. Others are quick to note that there have been many other reserve currencies throughout history, none of which have lasted more than a hundred and ten years, basically where the dollar is at now.

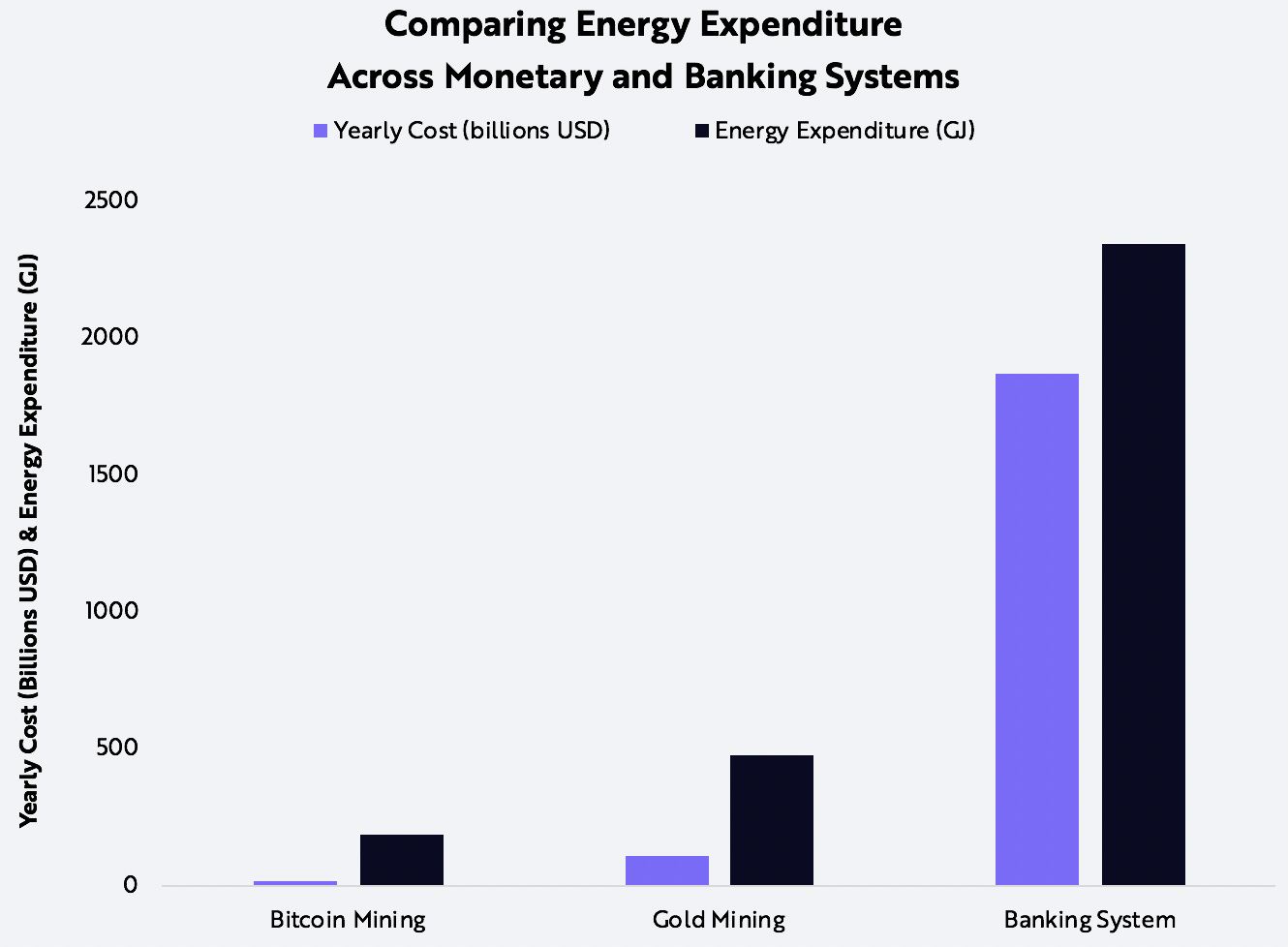

As any bitcoiner will tell you, it is the world’s first truly scarce asset. Unlike fiat currency, it is deflationary. And its source code and algorithmic emissions supply ensures that an increase in demand cannot lead to an increase in supply, unlike precious metals or any other commodity. I’ll also note here that despite ongoing environmental concerns that bitcoin will “boil the oceans”, the network currently uses less electricity than global gold production and a fraction of what other monetary networks use.

My point here is for you to consider what happens when there is infinite demand for a scarce asset? Number go up. Now I’m not going to speculate on whether bitcoin will replace the US dollar as the reserve currency in the next five to ten years, but I’m certainly not planning on selling any of my bitcoin right now, if ever. In fact, one of the reasons that I remain so bullish long term is the prevalence of lending platforms that allow people to use their bitcoin or other crypto assets as collateral to take out fiat loans. For what’s the point of selling an asset that goes up two hundred percent a year if you can lend it out to buy a house or other large purchase and have the loan pay itself back in two or four years? Yes, this is really something you can do in DeFi right now.

“If you want to make God laugh, tell him your plans.”

There’s another effect that seems to be inherent to getting involved with bitcoin: a low time preference. Individuals with low time preferences tend to favor their current well being, spending money and resources on today rather than on future well being. And “stacking sats”, or buying bitcoin and holding it through a multi-year downturn requires a different type of mindset than most people who are caught up in a debt-driven consumer culture. My parents weren’t able to provide me with a solid financial education, neither did public education, but you know who did? Bitcoiners.

And it may just be that I’m approaching my forty-second birthday, but I have been spending a lot of time thinking about my childrens’ future as well as what they call inter-generational wealth. We’ve even started having monthly meetings at the kitchen table to discuss the “family business”. We’re not completely financially independent yet, we still have the issue of healthcare to worry about, but the fact that I’m even in a position to do what I’m doing today would have been unfathomable to me eight and a half years ago.

For now, I’m going to continue writing, helping guide people into the crypto ecosystem (and not get rekt,) and networking with like minded individuals. I’ve already had several opportunities that have come my way that I’ve passed on, and it’s nice to be in the position to do that. What’s more important to me right now is the chance to spend the summer with the girls, and do a bit of travelling now that COVID restrictions are lightening up. But what I’m really looking forward to is the ability to do some deep work, to be able to sit down for hours at a stretch and work on a project without interruption from a phone call or text message. The work phone is already off my desk, and this article will be going out by my self-imposed deadline, as planned.

Wrapping up, I just want to say that if you're not allocating at least 1-5% of your net worth into Bitcoin, you're probably not gonna make it. Feel free to reach out in the comments if you have questions or want help implementing a dollar cost averaging plan to buy Bitcoin or Ethereum. Stay away from everything else until you know what you’re doing.

Until next time,

Michael